To Mega Caps or Ex Mega Caps: is that the question?

Summary

Share

Marketing communication

Key takeaways

• The rise of Mega Cap stocks1 has fundamentally reshaped the US equity market. These giants offer significant growth potential but also come with concentration risks that investors must carefully manage.

• By strategically allocating investments between the MSCI USA Mega Cap Select Index and the MSCI USA Ex Mega Cap Select Index, investors can balance the benefits of exposure to market leaders with the diversification2 needed to mitigate risk.

• Ultimately, the allocation of your US equity exposure should align with your unique goals, risk tolerance, and market outlook. Each investor must define their strategy based on their convictions, ensuring it reflects their priorities and adapts to the evolving equity landscape.

1. The phenomenal rise of Mega Cap stocks

Over the past decade, Mega Cap stocks have delivered extraordinary growth3. Companies like Apple, which surpassed a $3 trillion market valuation in 20244, and tech leaders Microsoft and Alphabet have consistently driven market returns through innovation and strong earnings performance5.

The numbers speak for themselves: over the past five years, the MSCI USA Mega Cap Select Index delivered an impressive annualised performance of 18%, far outpacing the broader MSCI USA Index at 15%6. This remarkable performance has solidified the dominance of Mega Caps in the market, but it also has significant implications for investors.

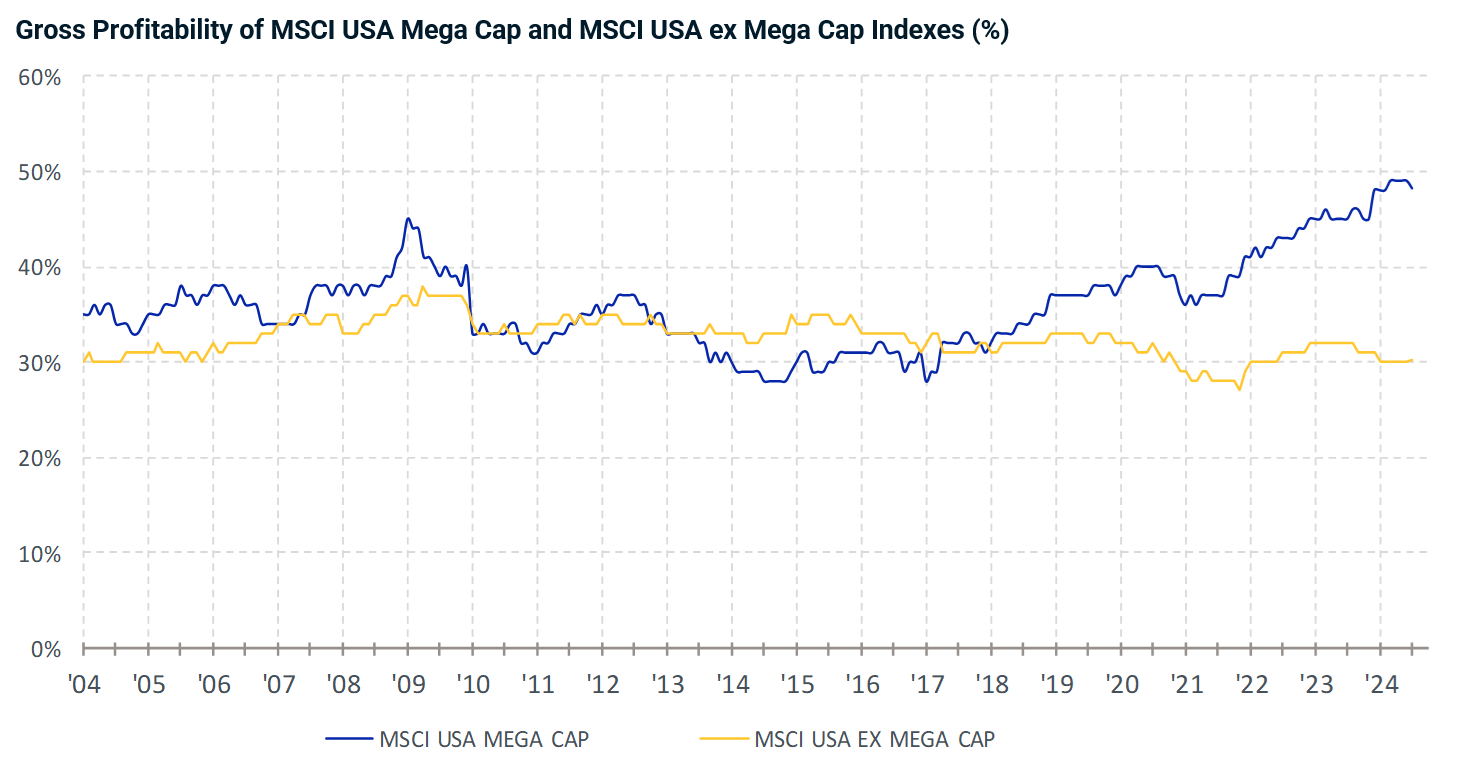

Source: MSCI, Gross Profitability is calculated as (Sales – Cost of Goods Sold)/Total Assets. Please refer to MSCI Fundamental Data Methodology Book, June 2024.

Source: Amundi, MSCI, Data as at 30/09/2024. Past performance is not a reliable indicator of future performance.

The risks behind the success

Mega-cap stocks, while undeniably successful, can pose risks to investors due to their outsized influence on market-cap-weighted indices. These indices have become increasingly concentrated in a few dominant companies. The MSCI USA Mega Cap Select Index, for example, trades at an average price-to-earnings (P/E) ratio of 32x, compared to 23.6x for the broader market, as measured by the MSCI USA Index6.

While these high valuation levels reflect strong growth prospects and investor confidence, they also make these stocks more vulnerable to market corrections.

2. The case for Mega Cap exposure

Mega Caps can of course play a critical role in a well-balanced portfolio:

- Market leadership: These companies are often leaders in innovation and hold dominant positions in sectors like technology, healthcare, and e-commerce.

- Resilience: Mega Caps generally have strong balance sheets and are often better positioned to withstand economic downturns.

- Megatrends: Investing in Mega Caps allows investors to benefit from ongoing trends such as digitalisation, artificial intelligence, and renewable energy.

Diversifying2 beyond Mega Caps

However, as discussed, while Mega Caps offer significant opportunities, they also introduce concentration risks. With this in mind, allocating to the MSCI USA Ex Mega Cap Index can provide diversification2 benefits by spreading exposure across mid-cap and smaller large-cap companies. These companies have often delivered higher performance during specific market cycles, driven by their agility and greater exposure to growth opportunities3.

For example, in 2023, the MSCI World ex USA Index—which excludes US Mega Cap stocks—posted a strong performance of 18.60%7, underscoring the potential merits of diversifying2 beyond Mega Caps to capture growth in other segments of the market3.

Diversifying2 beyond Mega Caps can:

- Mitigate sector-specific risks (e.g., technology overexposure).

- Reduce volatility by spreading investments across different market capitalisations and sectors.

- Provide access to the higher growth potential found in smaller, more agile companies.

A look at non-Mega Cap valuations

Non-Mega Cap stocks often trade at more attractive valuations, offering compelling opportunities for investors3.

These lower valuations could provide a margin of safety by reducing the risk of overpaying for future earnings and limiting downside potential in volatile markets, while offering better upside potential, as valuations revert to historical averages.

To Mega Caps or Ex Mega Caps?

The debate between concentration and diversification2 lies at the heart of investment strategy. When it comes to Mega Cap and non-Mega Cap stocks, the decision ultimately hinges on each investor’s unique priorities and approach.

Mega Cap stocks may continue to lead in innovation and market influence, while smaller-cap companies can offer distinct opportunities for diversification and growth2. The right choice depends on your individual goals, risk tolerance, and outlook for the market.

Each investor must craft their allocation strategy thoughtfully, aligning it with their convictions and adapting it to the evolving equity landscape.

3. Accessing the opportunity

ETFs can provide simple and cost-effective access to US equities.

The Amundi MSCI USA Mega Cap UCITS ETF offers exposure to the largest securities with a market capitalization above $200 Bn within the MSCI USA Index (currently 37 stocks including the so-called “Magnificent 7”)8. It is suitable for investors seeking growth potential from US Mega Cap stocks3.

The Amundi MSCI USA Ex Mega Cap UCITS ETF offers exposure to the broader MSCI USA index while excluding the constituents of the MSCI USA Mega Cap Select Index8. This allows investors to diversify their US exposure and reduce correlation with the performance of the US Mega Cap stocks9.

1.Mega Cap stocks are defined as companies with market capitalisations in excess of $200 billion.

2.Diversification does not guarantee a profit or protect against a loss.

3.Past market trends are not a reliable indicator of future ones.

4.https://www.forbes.com/sites/dereksaul/2024/10/15/apple-stock-rises-to-all-time-high-and-record-36-trillion-market-cap/

5.Past performance is not a reliable indicator of future performance.

6.Source: Bloomberg, MSCI, Amundi, Data as at 31/10/2024. Past performance is not indicative of future returns.

7.Source: MSCI World ex USA Index factsheet as at 31/12/2023.

8.As of 27/11/2024. For more details regarding the investment objective of the fund, please refer to the Key Information (KID) and the prospectus. For more information regarding the index methodology, please refer to msci.com.

9.Diversification does not guarantee a profit or protect against a loss. Please note that the fund does not offer any capital or performance guarantee.

Investment involves risks. For more information, please refer to the Risk section below.

KNOWING YOUR RISK

It is important for potential investors to evaluate the risks described below and in the fund’s Key Information Document (“KID”) and prospectus available on our website www.amundietf.com.

CAPITAL AT RISK - ETFs are tracking instruments. Their risk profile is similar to a direct investment in the underlying index. Investors’ capital is fully at risk and investors may not get back the amount originally invested.

UNDERLYING RISK - The underlying index of an ETF may be complex and volatile. For example, ETFs exposed to Emerging Markets carry a greater risk of potential loss than investment in Developed Markets as they are exposed to a wide range of unpredictable Emerging Market risks.

REPLICATION RISK - The fund’s objectives might not be reached due to unexpected events on the underlying markets which will impact the index calculation and the efficient fund replication.

COUNTERPARTY RISK - Investors are exposed to risks resulting from the use of an OTC swap (over-the-counter) or securities lending with the respective counterparty(-ies). Counterparty(-ies) are credit institution(s) whose name(s) can be found on the fund’s website amundietf.com. In line with the UCITS guidelines, the exposure to the counterparty cannot exceed 10% of the total assets of the fund.

CURRENCY RISK – An ETF may be exposed to currency risk if the ETF is denominated in a currency different to that of the underlying index securities it is tracking. This means that exchange rate fluctuations could have a negative or positive effect on returns.

LIQUIDITY RISK – There is a risk associated with the markets to which the ETF is exposed. The price and the value of investments are linked to the liquidity risk of the underlying index components. Investments can go up or down. In addition, on the secondary market liquidity is provided by registered market makers on the respective stock exchange where the ETF is listed. On exchange, liquidity may be limited as a result of a suspension in the underlying market represented by the underlying index tracked by the ETF; a failure in the systems of one of the relevant stock exchanges, or other market-maker systems; or an abnormal trading situation or event.

VOLATILITY RISK – The ETF is exposed to changes in the volatility patterns of the underlying index relevant markets. The ETF value can change rapidly and unpredictably, and potentially move in a large magnitude, up or down.

CONCENTRATION RISK – Thematic ETFs select stocks or bonds for their portfolio from the original benchmark index. Where selection rules are extensive, it can lead to a more concentrated portfolio where risk is spread over fewer stocks than the original benchmark.

CREDIT WORTHINESS – The investors are exposed to the creditworthiness of the Issuer.

IMPORTANT INFORMATION

This material is solely for the attention of professional and eligible counterparties, as defined in Directive MIF 2014/65/UE of the European Parliament (where relevant, as implemented into UK law) acting solely and exclusively on their own account. It is not directed at retail clients. In Switzerland, it is solely for the attention of qualified investors within the meaning of Article 10 paragraph 3 a), b), c) and d) of the Federal Act on Collective Investment Scheme of June 23, 2006.

This information is not for distribution and does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any U.S. Person (as defined in the prospectus of the Funds or in the legal mentions section on www.amundi.com and www.amundietf.com. The Funds have not been registered in the United States under the Investment Company Act of 1940 and units/shares of the Funds are not registered in the United States under the Securities Act of 1933.

This document is of a commercial nature. The funds described in this document (the “Funds”) may not be available to all investors and may not be registered for public distribution with the relevant authorities in all countries. It is each investor’s responsibility to ascertain that they are authorised to subscribe, or invest into this product. Prior to investing in the product, investors should seek independent financial, tax, accounting and legal advice.

This is a promotional and non-contractual information which should not be regarded as an investment advice or an investment recommendation, a solicitation of an investment, an offer or a purchase, from Amundi Asset Management (“Amundi”) nor any of its subsidiaries.

The Funds are Amundi UCITS ETFs. The Funds can either be denominated as “Amundi ETF” or “Lyxor ETF”. Amundi ETF designates the ETF business of Amundi.

Amundi UCITS ETFs are passively-managed index-tracking funds. The Funds are French, Luxembourg or Irish open ended mutual investment funds respectively approved by the French Autorité des Marchés Financiers, the Luxembourg Commission de Surveillance du Secteur Financier or the Central Bank of Ireland, and authorised for marketing of their units or shares in various European countries (the Marketing Countries) pursuant to the article 93 of the 2009/65/EC Directive.

The Funds can be French Fonds Communs de Placement (FCPs) and also be sub-funds of the following umbrella structures:

For Amundi ETF:

- Amundi Index Solutions, Luxembourg SICAV, RCS B206810, located 5, allée Scheffer, L-2520, managed by Amundi Luxembourg S.A.

- Amundi ETF ICAV: open-ended umbrella Irish collective asset-management vehicle established under the laws of Ireland and authorized for public distribution by the Central Bank of Ireland. The management company of the Fund is Amundi Ireland Limited, 1 George’s Quay Plaza, George’s Quay, Dublin 2, D02 V002, Ireland. Amundi Ireland Limited is authorised and regulated by the Central Bank of Ireland

Before any subscriptions, the potential investor must read the offering documents (KID and prospectus) of the Funds. The prospectus in French for French UCITS ETFs, and in English for Luxembourg UCITS ETFs and Irish UCITS ETFs, and the KID in the local languages of the Marketing Countries are available free of charge on www.amundi.com, www.amundi.ie or www.amundietf.com. They are also available from the headquarters of Amundi Luxembourg S.A. (as the management company of Amundi Index Solutions), or the headquarters of Amundi Asset Management (as the management company of Amundi ETF French FCPs, Multi Units Luxembourg, Multi Units France and Lyxor Index Fund), or at the headquarters of Amundi Ireland Limited (as the management company of Amundi ETF ICAV). For more information related to the stocks exchanges where the ETF is listed please refer to the fund’s webpage on amundietf.com.

Investment in a fund carries a substantial degree of risk (i.e. risks are detailed in the KID and prospectus). Past Performance does not predict future returns. Investment return and the principal value of an investment in funds or other investment product may go up or down and may result in the loss of the amount originally invested. All investors should seek professional advice prior to any investment decision, in order to determine the risks associated with the investment and its suitability.

It is the investor’s responsibility to make sure his/her investment is in compliance with the applicable laws she/he depends on, and to check if this investment is matching his/her investment objective with his/her patrimonial situation (including tax aspects).

Please note that the management companies of the Funds may de-notify arrangements made for marketing as regards units/shares of the Fund in a Member State of the EU or the UK in respect of which it has made a notification.

A summary of information about investors’ rights and collective redress mechanisms can be found in English on the regulatory page at https://about.amundi.com/Metanav-Footer/Footer/Quick-Links/Legal-documentation with respect to Amundi ETFs.

This document was not reviewed, stamped or approved by any financial authority.

This document is not intended for and no reliance can be placed on this document by persons falling outside of these categories in the below mentioned jurisdictions. In jurisdictions other than those specified below, this document is for the sole use of the professional clients and intermediaries to whom it is addressed. It is not to be distributed to the public or to other third parties and the use of the information provided by anyone other than the addressee is not authorised.

This material is based on sources that Amundi and/or any of her subsidiaries consider to be reliable at the time of publication. Data, opinions and analysis may be changed without notice. Amundi and/or any of her subsidiaries accept no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi and/or any of her subsidiaries can in no way be held responsible for any decision or investment made on the basis of information contained in this material.

Updated composition of the product’s investment portfolio is available on www.amundietf.com. Units of a specific UCITS ETF managed by an asset manager and purchased on the secondary market cannot usually be sold directly back to the asset manager itself. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them.

Indices and the related trademarks used in this document are the intellectual property of index sponsors and/or its licensors. The indices are used under license from index sponsors. The Funds based on the indices are in no way sponsored, endorsed, sold or promoted by index sponsors and/or its licensors and neither index sponsors nor its licensors shall have any liability with respect thereto. The indices referred to herein (the “Index” or the “Indices”) are neither sponsored, approved or sold by Amundi nor any of its subsidiaries. Neither Amundi nor any of its subsidiaries shall assume any responsibility in this respect.

AMUNDI PHYSICAL GOLD ETC (the “ETC”) is a series of debt securities governed by Irish Law and issued by Amundi Physical Metals plc, a dedicated Irish vehicle (the “Issuer”). The Base Prospectus, and supplement to the Base Prospectus, of the ETC has been approved by the Central Bank of Ireland (the “Central Bank”), as competent authority under the Prospectus Directive. Pursuant to the Directive Prospective Regulation, the ETC is described in a Key Information Document (KID), final terms and Base Prospectus (hereafter the Legal Documentation). The ETC KID must be made available to potential subscribers prior to subscription. The Legal Documentation can be obtained from Amundi on request. The distribution of this document and the offering or sale of the ETC Securities in certain jurisdictions may be restricted by law. For a description of certain restrictions on the distribution of this document, please refer to the Base Prospectus. The investors are exposed to the creditworthiness of the Issuer.

In EEA Member States, the content of this document is approved by Amundi for use with Professional Clients (as defined in EU Directive 2004/39/EC) only and shall not be distributed to the public.

Information reputed exact as of the date mentioned above.

Reproduction prohibited without the written consent of Amundi.